ABLE Accounts: What Most Caregivers Get Wrong (And How to Fix It)

Did you know that over 8 million Americans qualify for an ABLE account, yet as of December 2024, only 187,000 accounts have been opened nationwide?

That means roughly 2.3% of eligible individuals are actually using this powerful financial tool. This massive gap highlights the need for more awareness and education about ABLE accounts., yet the vast majority aren’t using one? Why? Because there’s a mountain of bad information floating around that’s keeping people from taking advantage of this powerful financial tool.

Wait! What? You don’t know or aren’t exactly sure what an ABLE account is? You’re not alone. There’s a lot of confusion around these accounts—some people think they’re only for kids, others assume they’ll mess with government benefits, and plenty of folks don’t even know they exist. Hence why only 2.3% have opened one!

Let’s clear things up. There was a time in my life when I had no idea it even existed.

Here’s the skinny: An ABLE (Achieving a Better Life Experience) account is a tax-advantaged savings account designed for people with disabilities. It allows them to save money without jeopardizing their eligibility for critical government benefits like SSI (Supplemental Security Income) and Medicaid. The best part? The money grows tax-free, and it can be used for a wide range of expenses, from housing and education to transportation and healthcare.

Now, what actually counts as a disability for an ABLE account? Certainly many physical disabilities, but not all neurodivergent conditions automatically qualify—eligibility depends on the severity of functional limitations.

To qualify, a person must have developed a significant disability before the age of 26 and meet the Social Security Administration’s definition of a “significant functional limitation.” Since Divergent Money is all about neurodivergence, let’s get specific. To qualify, a person must have developed a significant disability before the age of 26. This includes a wide range of conditions, such as:

- Autism spectrum disorder (ASD)

- ADHD (if it significantly impacts daily functioning)

- Intellectual disabilities

- Cerebral palsy

- Epilepsy

- Blindness or significant vision impairment

- Hearing loss

- Mental health disorders like schizophrenia or severe depression

- Neurological conditions like multiple sclerosis or muscular dystrophy

The disability must either qualify for SSI or SSDI OR meet the Social Security Administration’s definition of “significant functional limitations.” If you’re not sure whether your loved one qualifies, checking with a medical provider or reviewing the SSA’s Blue Book can help.

Let’s cut through the nonsense. If you’re a caregiver, parent, or advocate for someone with a disability, you need to know the truth. Here are the five biggest myths about ABLE accounts—and exactly how to stop them from holding you back.

MYTH #1: "ABLE Accounts Will Affect Government Benefits"

🚨 The Misconception: If I open an ABLE account, my loved one will lose access to SSI, Medicaid, or other government programs.

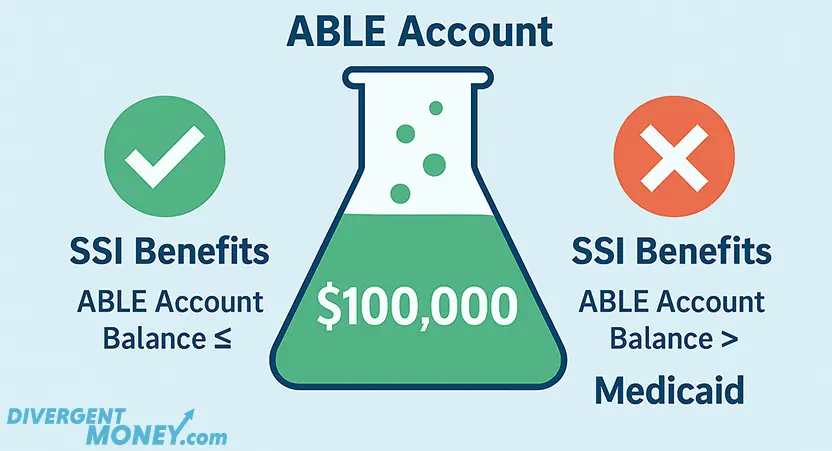

✅ The Reality: ABLE accounts are designed NOT to count against the $2,000 asset limit for Supplemental Security Income (SSI) or other government benefits. In fact, you can have up to $100,000 in an ABLE account without affecting SSI eligibility at all.

⚠️ Important Note: If an ABLE account balance exceeds $100,000, SSI payments may be temporarily suspended—but Medicaid eligibility remains intact. Once the balance is below $100,000, SSI payments resume.

💡 How to Fix It:

- ABLE accounts were created specifically so people with disabilities can save money without risking their benefits.

- Funds in an ABLE account are legally protected from asset tests in most cases.

Pro Tip: Need proof? The Social Security Administration (SSA) confirms this in their official guidelines.

MYTH #2: "ABLE Accounts Are Only for Kids"

🚨 The Misconception: These accounts are for young children or teenagers, right?

✅ The Reality: Nope. If someone was diagnosed with a qualifying disability before the age of 26, they’re eligible to open an ABLE account at any age—whether they’re 5, 15, or 55.

🔹 Advocacy Note: BIG CHANGES ARE COMING! Starting January 1, 2026, the eligibility criteria for ABLE accounts will expand to include individuals whose disability began before age 46, potentially adding another 6 million eligible Americans. This expansion makes it even more critical to spread awareness about the benefits of ABLE accounts., which could expand eligibility for more adults with later-diagnosed disabilities.

![TIMELINE SHOWING HOW ABLE ELIGIBILITY CAN APPLY TO OLDER ADULTS DIAGNOSED EARLY]](https://www.divergentmoney.com/content/images/2025/03/DM_ABLE_eligibility.png)

💡 How to Fix It:

- If your loved one was diagnosed before age 26, it doesn’t matter if they’re older now—they’re still eligible to open an ABLE account.

- Many adults with disabilities are using ABLE accounts to save money for housing, transportation, and long-term needs.

🎯 Example: A 40-year-old autistic adult diagnosed at age 3? Absolutely eligible.

MYTH #3: "I Can’t Afford to Contribute, So It’s Not Worth It"

🚨 The Misconception: I don’t have extra cash lying around, so what’s the point?

✅ The Reality: Even small contributions add up over time—especially since an ABLE account can grow tax-free.

💡 How to Fix It:

- You don’t have to max it out. Even $20/month builds savings and investment growth over time.

- Friends and family can contribute too! If they want to help, an ABLE account is a great place for holiday or birthday gifts.

- Many states have ABLE matching grant programs—free money for your loved one’s account.

📊 Example: If you put just $50/month into an ABLE account starting today, you could have over $6,000 in five years—without even counting investment growth.

MYTH #4: "It’s Just a Regular Savings Account"

🚨 The Misconception: An ABLE account is just a fancy bank account with more restrictions.

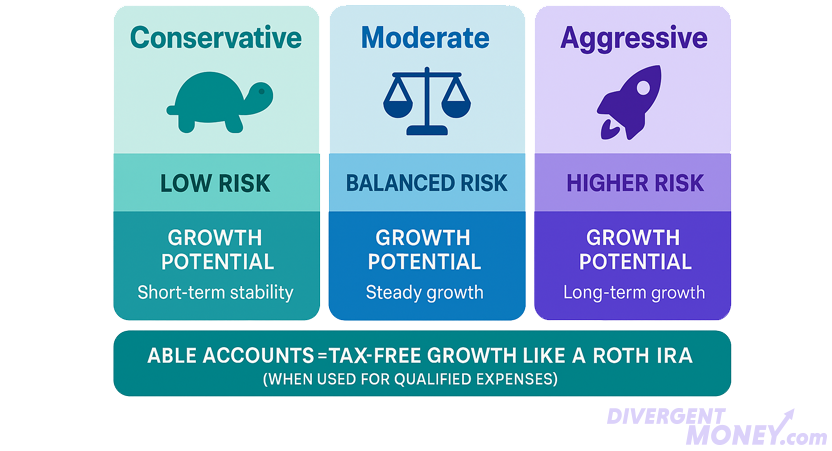

✅ The Reality: ABLE accounts can be invested, meaning your savings grow tax-free, similar to a Roth IRA. The biggest financial perk? Tax-free earnings and withdrawals when used for qualified expenses.

💡 How to Fix It:

- Most ABLE programs offer investment options that can help funds grow over time, including conservative, moderate, and aggressive portfolios.

- If you’re not sure how to invest, many ABLE accounts allow you to start safe with conservative options and adjust as needed.

- Understand contribution limits: The annual contribution limit for an ABLE account is $18,000 in 2024 (or higher if the beneficiary is working).

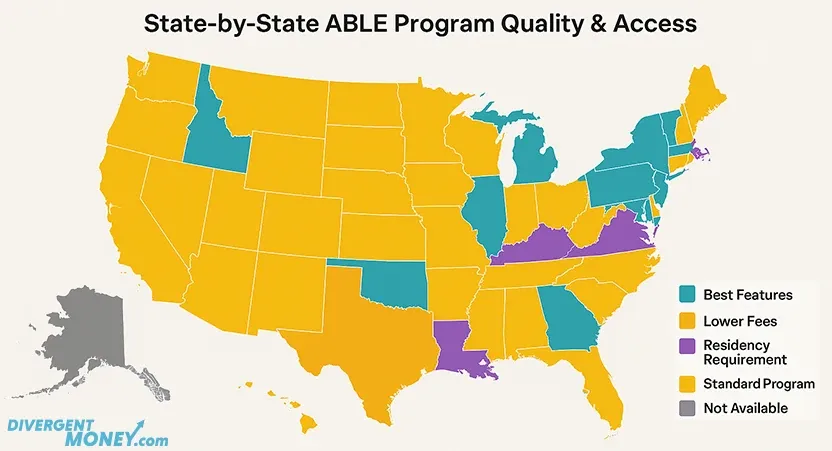

🔎 Want proof? Check out your state’s ABLE program website to compare investment choices.

💡 Investment Options Available:

- Conservative options (low-risk, stable growth)

- Moderate options (balanced risk and return)

- Aggressive growth options (higher potential returns for long-term investing)

🔹 Action Step: Check your state's ABLE program for specific investment choices and compare performance.

MYTH #5: "I Can Only Use ABLE Money for Medical Expenses"

🚨 The Misconception: I’ll have to jump through a million hoops just to use the money for anything other than doctor visits.

✅ The Reality: ABLE accounts cover a LOT more than just medical bills. The official term is Qualified Disability Expenses (QDEs), and they include:

- Housing & rent 🏠

- Transportation 🚗 (yes, including buying a car)

- Education 🎓 (tuition, books, online courses)

- Assistive technology 💻 (laptops, communication devices)

- Job training 👩🏫

- Legal & financial planning 📑

- Personal support services 🧑⚕️

💡 How to Fix It:

- Think bigger than just medical bills. ABLE funds can help improve quality of life, not just cover hospital costs.

- If it helps the individual live, work, or maintain their independence, it likely counts as a qualified expense.

- Keep good records—tracking expenses ensures compliance and prevents any potential IRS or benefit issues.

🎯 Example: You can use ABLE money to buy a service dog, pay for Uber rides, or even cover rent in many cases.

Caregivers, Don’t Leave Money on the Table

ABLE accounts exist to give people with disabilities financial freedom—yet so many families miss out because of misinformation.

🔥 Here’s what you should do next:

✅ **Check if your loved one qualifies (spoiler: if you've made it past our gauntlet of caveats, they probably do). If you're unsure, eligibility often depends on functional limitations, not just diagnosis. If your loved one qualifies for SSI/SSDI or meets the SSA’s definition of a 'significant functional limitation,' they can likely open an ABLE account.

✅ Compare state ABLE programs (some have lower fees & better investment options).

✅ Start small, but start now—even $20/month makes a difference.

🔗 Want more details? Check out these official resources:

Disclaimer: As ALWAYS, this article is for educational and motivational purposes and is not financial advice. Always consider consulting with a financial professional for guidance tailored to your unique situation.