Welcome to the Matrix. The Divergent Money Matrix!

At Divergent Money, we're always moving towards solutions, towards understanding.

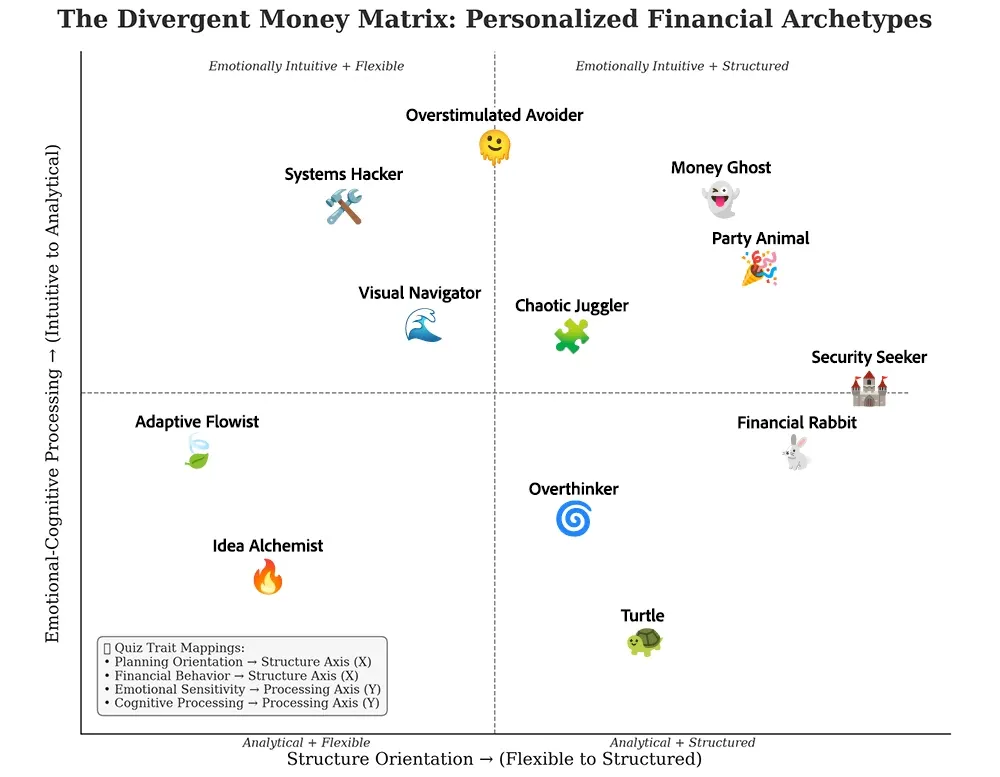

And so, we present to you... the Divergent Money Matrix, a map to help chart a path to greater self knowledge. Let's take a look.

The Divergent Money Matrix (DMM) applies engineering rigor to personal finance, helping us dissect how cognitive diversity interacts with money management. Traditional financial advice oversimplifies, but the DMM reveals a deeper truth: success with money isn’t just about knowledge—it’s about alignment between how you think and the financial systems you use. Most importantly, we've come up with cute names to help you remember them!

If you’ve ever felt like traditional budgeting advice just doesn’t work for you, congratulations—you’re human, and also why you're here. Money isn’t a one-size-fits-all game, yet most financial advice assumes there’s a “correct” way to manage it.

Enter the Divergent Money Matrix —a tool designed to help you get to the bottom of your unique relationship with money based on how your brain processes information.

Ready to take the red pill?

Booting Up the Divergent Money Matrix

Think of the DMM as a grid that maps how different cognitive styles interact with core financial tasks. It helps us pinpoint why money management can feel intuitive for some, frustrating for others, and downright impossible for those of us who don’t fit the neurotypical mold.

The DMM looks at two key dimensions:

- How we think – Our cognitive processing styles, including how we perceive, organize, and act on financial information.

- What we need to do – The essential financial tasks that apply to everyone, from tracking spending to planning for the future.

When these dimensions intersect, we get a powerful map of financial cognition—showing both where we struggle and where we have hidden strengths.

How Your Brain Interacts with Money

Different brains process information in different ways. That’s not a flaw; it’s a feature. The problem? The financial system was built with only a few of these processing styles in mind.

Here are some common cognitive patterns and how they impact financial behavior:

- Pattern Spotters – See trends before others, making them great at recognizing spending habits and investment opportunities. But they may overlook small details, like recurring subscriptions.

- Burst Processors – Work best in hyper-focused sprints, excelling at short-term financial projects. Traditional “daily tracking” methods? A nightmare.

- Visual Thinkers – Understand information best through charts, graphs, and images rather than raw numbers or spreadsheets.

- High-Sensory Brains – Easily overwhelmed by too much financial noise (complex banking apps, endless transaction lists), often leading to avoidance.

- Abstract Planners – Love big-picture strategy but struggle with execution (e.g., they know they need an emergency fund but can’t get themselves to automate it).

Notice how none of these are inherently bad? Yet, financial systems assume that only certain cognitive styles are 'correct,' forcing everyone else to struggle. Take traditional budgeting apps: they're built for a singular way of thinking—linear, detail-oriented, and hyper-consistent. But what about those who process information in bursts? Or those who need a visual-first approach? Instead of adapting tools to fit diverse minds, most financial systems demand conformity—and that’s where they fall short. Emerging solutions, however, are starting to change this narrative, offering more flexible, intuitive, and customizable financial management options. Instead of adapting tools to fit diverse minds, the system demands conformity—and that’s where it fails. Yet, if financial systems aren’t built to accommodate different styles, they create unnecessary struggles.

The Four Core Money Skills Everyone Needs

Regardless of how we think, financial success boils down to four essential skills:

- Perceive – Accurately process financial information (understand your bank statements, recognize spending patterns, assess investment options).

- Plan – Set financial goals and structure systems to achieve them (budgeting, saving, strategizing for long-term wealth).

- Execute – Take action (pay bills, make purchases, move money, stick to plans).

- Evaluate – Track progress, learn from past mistakes, and adjust accordingly.

So far, so good—until we realize that most financial tools assume one way of achieving these goals. But what if we flipped the script?

How the Divergent Money Matrix Changes the Game

When we overlay cognitive styles with financial tasks, the FCM reveals something powerful:

- Hidden Strengths:

- A pattern-spotter who struggles with budgets might excel at recognizing market trends—meaning investing could be their financial sweet spot.

- A burst-processor who forgets to check their account daily might thrive with an automated weekly financial check-in.

- Unnecessary Barriers:

- Many financial struggles aren’t personal failures—they’re signs that the system wasn’t designed with cognitive diversity in mind.

- Example: If someone avoids budgeting apps because they find endless transaction lists overwhelming, the problem isn’t them—it’s the lack of a visually intuitive system.

- Better Solutions:

- Financial tools should adapt to you, not the other way around.

- The ideal budgeting app for a visual thinker? Heavy on graphs and infographics.

- For a high-sensory brain? Clean, simple interfaces with minimal notifications.

- For a burst processor? A gamified system that rewards quick sprints of financial engagement.

The Future of Finance: Smarter, More Adaptive, and Built for Everyone

Imagine a financial world where:

- Budgeting apps adjust their display based on your preferred information style.

- Investment platforms offer insights in text, visuals, or interactive simulations.

- Money management tools recognize your natural motivation patterns and use them to drive engagement.

This isn’t just a dream—it’s the next evolution of financial tech. The Divergent Money Matrix gives us a framework to rethink how we design tools, making finance more accessible, intuitive, and actually usable for everyone.

Because the problem isn’t your brain.

The problem is that finance wasn’t built for it—yet. But change is happening. AI-driven budgeting assistants, adaptive banking interfaces, and neurodivergent-friendly financial planning tools are emerging to bridge the gap. The next generation of money management will be designed for all minds, not just those that fit traditional financial models. But change is coming. Emerging financial tools like AI-driven budgeting assistants, neurodivergent-friendly banking interfaces, and adaptive financial planning apps are starting to bridge the gap. The next generation of money management will be designed for all minds, not just the ones that fit into traditional models.

In our next article on the Divergent Money Matrix, we'll go deeper and decode each type, how they align with different personalities, and offering insights and strategies to optimize personal finance.

Disclaimer: As ALWAYS, this article is for educational and motivational purposes and is not financial advice. Always consider consulting with a financial professional for guidance tailored to your unique situation.